1 July 2024

In the year since the term was coined by Bank of America strategist Michael Hartnett, market participants have become obsessed with the “Magnificent 7”, a small handful of technology related stocks whose blistering performance has dominated both in terms of market capitalisation and returns.

But what are the Magnificent 7 and why have they done so well?

To answer these questions, we first need to know both what these companies do and what has driven them to become such large components of the index.

The Magnificent 7 are a very diverse group of businesses, despite what may be written in the mainstream press. Tesla is a car manufacturer; Apple makes personal electronic devices; Alphabet is an advertising business; Amazon is a retailer and cloud computing platform; Microsoft is a software and cloud computing business, whilst Nvidia is a manufacturer of advanced semiconductors enabling the AI revolution. Whilst they are all clearly connected by technology (indeed most businesses in the 21st century are to an extent), they all have very different business models, some of which are more attractive than others. They all therefore have their own unique drivers of growth in earnings and cash flows that to us is the ultimate determinant of share price performance over the long term.

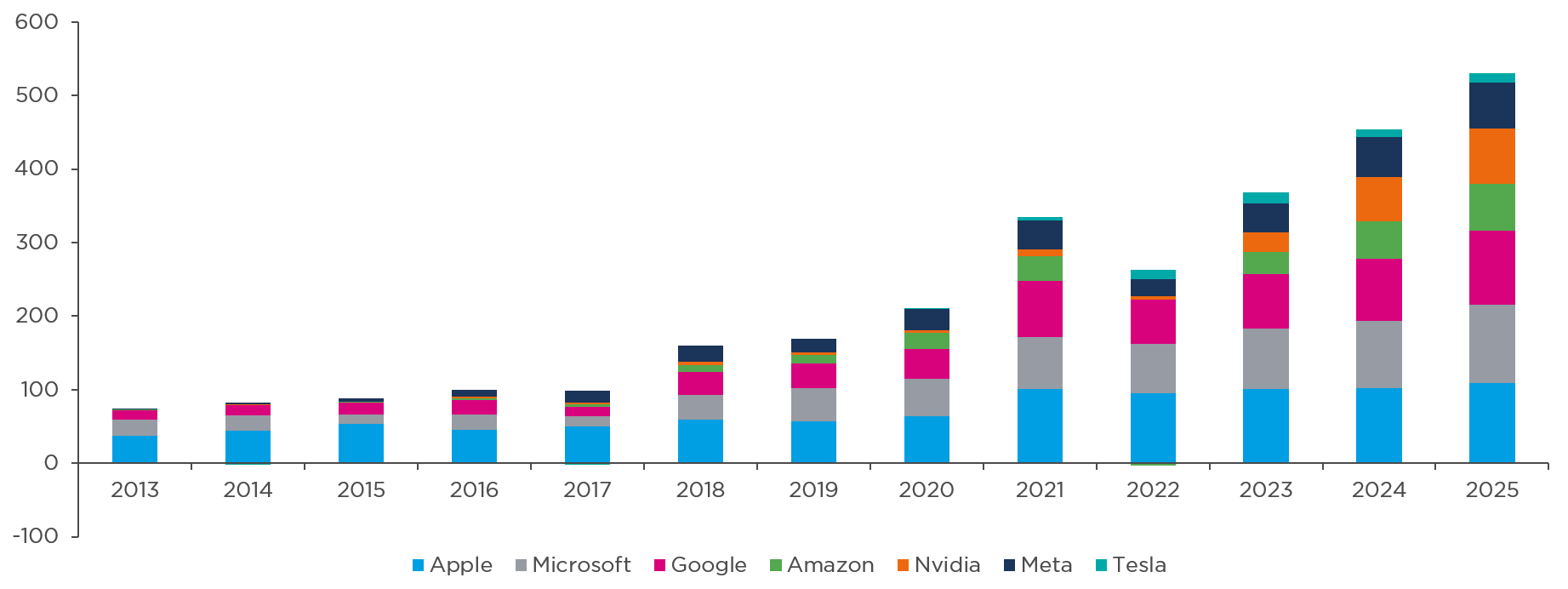

This brings us to the question; why have they performed so well? The answer is simple. It is in large part due to compound growth in earnings and cash flows. The chart below shows the annual net profits for this group of companies over the last 10 years, indicating that they have shown considerable growth in profits. Microsoft, for example, has seen profits grow 5-fold from $22bn to $106bn whilst more recently, Nvidia has been the stand-out performer with net income rising from $4bn in 2022 to $56bn in 2024, a 10-fold rise in little more than a year.

Why have technology companies performed so well?

Source: CCLA and Bloomberg, as at 31 March 2024.

This, along with the corresponding performance of the stocks, has led to high levels of market concentration. Nvidia, Microsoft, Apple, Amazon, Meta and Alphabet account for over 25% of the US stock market in terms of market capitalisation and are expected to produce over 20% of the net income in 2024.1

So why don’t we own all these stocks at such high concentration in CCLA equity portfolios?

At CCLA, when we build portfolios, we do not start with the index and work backwards; we start from the bottom up, with the expected returns available from across the opportunity set. We seek to build well diversified portfolios of high-quality businesses, well positioned to grow and compound earnings and cash flows over the long term and trading at reasonable valuations. This means that we do not hold companies just because they are a large component of the benchmark.

Tesla is one of the stocks in the Magnificent 7 that we do not own. Whilst we recognise that Electric Vehicles (EVs) are likely to continue to gain share in car production over time, we see the business model and competitive dynamics within the industry as unattractive. Car manufacturing is a capital-intensive business, meaning that the business has to invest large amounts of shareholder capital in order to generate growth. In addition, there is significant competition, both from established, developed market car manufacturers, but also from Chinese companies that typically have cost advantages in manufacturing. This has more recently manifested itself in a price war in the industry. Corporate governance is also a concern, not least the eye watering renumeration package recently approved for the CEO Elon Musk.

Apple is another company that is not held in CCLA portfolios. Whilst the company has a strong brand and high-quality products, we view smartphone usage in developed markets as a mature industry, and the company has failed to deliver any real innovation for the customer in over a decade. As a result, consumers now hold onto their handsets for longer than ever before, which creates headwinds to growth for the business. The future development of AI products and services integrated into handsets may well augment this thesis, but this has yet to be seen.

We do hold positions in Microsoft, Nvidia, Amazon & Alphabet. However, in order to ensure diversification within our portfolios, these positions are smaller than found in market benchmarks. This has led to the group of stocks remaining a headwind to equity performance over the last year.

Nvidia in particular has been painful on a relative performance basis, with the stock rising over 150% this year2 as the company continues to show dramatic growth in earnings as the major technology companies race to build out the infrastructure needed to train and run AI models. However, Nvidia has a track record of being highly cyclical, operates in end markets that are inherently unpredictable and we see no reason to believe that this time is different. For that reason, we prefer a modest position in the stock, and we remain wary of a slowdown in growth and the likely share price volatility that this would bring. As such, we have reduced our position this year as the valuation has expanded and to manage overall levels of risk within portfolios.

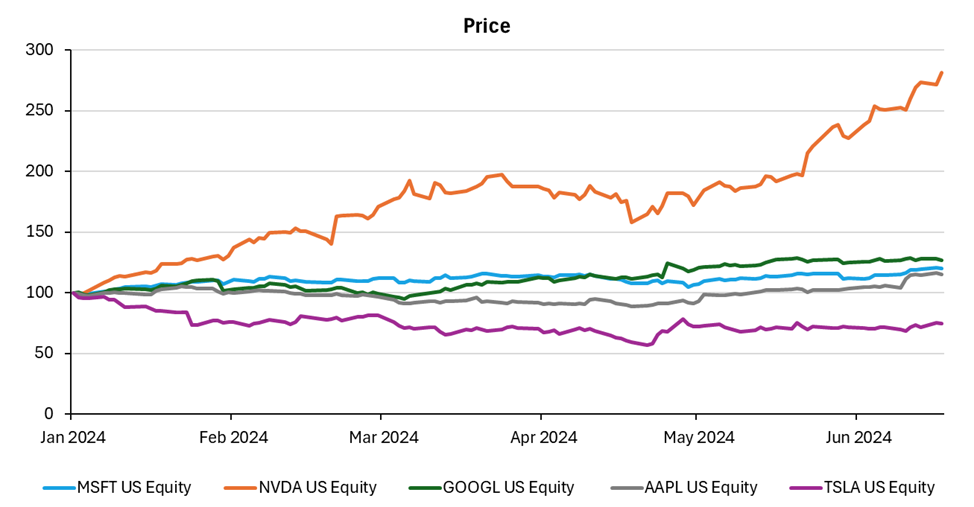

The chart below outlines the divergent performance of the group year-to-date.

Source: Bloomberg, as at 18 June 2024.

Beyond the Magnificent 7

There is far more to the semiconductor industry, though than just Nvidia. As semiconductors become smaller and more advanced, an opportunity is created for other businesses in the supply chain. ASML for example, is a leader in lithography equipment used to manufacture semiconductors at the leading edge. They benefit not only from complexity but also from the drive by developed markets and the US in particular, to re-shore manufacturing and protect against political instability. Synopsys too is a big beneficiary of these trends. They are a leader in software used to design semiconductors, more of which is needed as they become smaller and more complicated. Finally, Broadcom benefits from the desire of companies within the technology industry to build their own custom chips (ASICS), as well as from growth in data centre investment more generally.

Likewise, just as we can get exposure to the semiconductor supply chain via niche businesses, so too can we get exposure to growth within electric vehicles without owning a car manufacturer, where the competitive dynamics are unfavourable. NXP Semiconductor is a leader in the supply of semiconductors to the automotive industry. They stand to benefit over the next 5-10 years as EV’s take up a greater share of car production, but also from the increased use of chips to facilitate safety, entertainment and even self-driving features in modern cars.

Beyond technology

Much has been made by market commentators regarding the contribution of the Magnificent 7 to overall growth in earnings at the market level. Given the size of these businesses and the level of growth on offer, there is no doubt that they have made a big contribution. However, this is only half of the story. Over the last year, several areas within the market have been in a downcycle, notably commodities, but also pharmaceuticals and healthcare equipment manufacturers as they suffer the hangover following significant growth during the covid pandemic. All of this noise masks a plethora of opportunities for growth for those investors willing to look beyond big tech and seek exposure to the wide range of secular growth opportunities available. For example, in the healthcare sector, ageing demographics and subsequent investment into research and development for novel therapies will benefit those in the supply chain. Companies such as Thermofisher and Danaher are key beneficiaries. In medical devices, companies such as Edwards Life Sciences and Stryker are rolling out innovative treatments in areas such as heart disease and robotic surgery. Meanwhile, within the industrials sector, the drive for greater energy efficiency will benefit those companies whose products enable companies and asset owners to reduce their carbon footprint. Examples in CCLA portfolios include Schneider Electric and Trane Technologies. Likewise, there remains a great opportunity for companies that provide data and analytics products to various industries, such as finance and legal, demonstrated by the attractive growth at business such as Relx, Experian and S&P Global.

Therefore, whilst AI is clearly an exciting opportunity and a number of companies in the Magnificent 7 continue to provide the opportunity for future growth, they are clearly not the only mechanisms by which investors can gain exposure to compound growth in earnings and cash flows. Indeed, the long-term beneficiaries of investment in AI may well prove to be the thousands of companies outside the technology ecosystem who can use AI to improve their efficiency, develop new products and create new consumer experiences.

At CCLA we will continue to look for a wide range of growth opportunities, keeping our focus on quality and reasonable valuations whilst ensuring portfolios are well diversified.