27 February 2025

Helen Luong, Portfolio Manager

'Diversification’, Nobel Laureate Harry Markowitz said, ‘is the only free lunch in investing'.

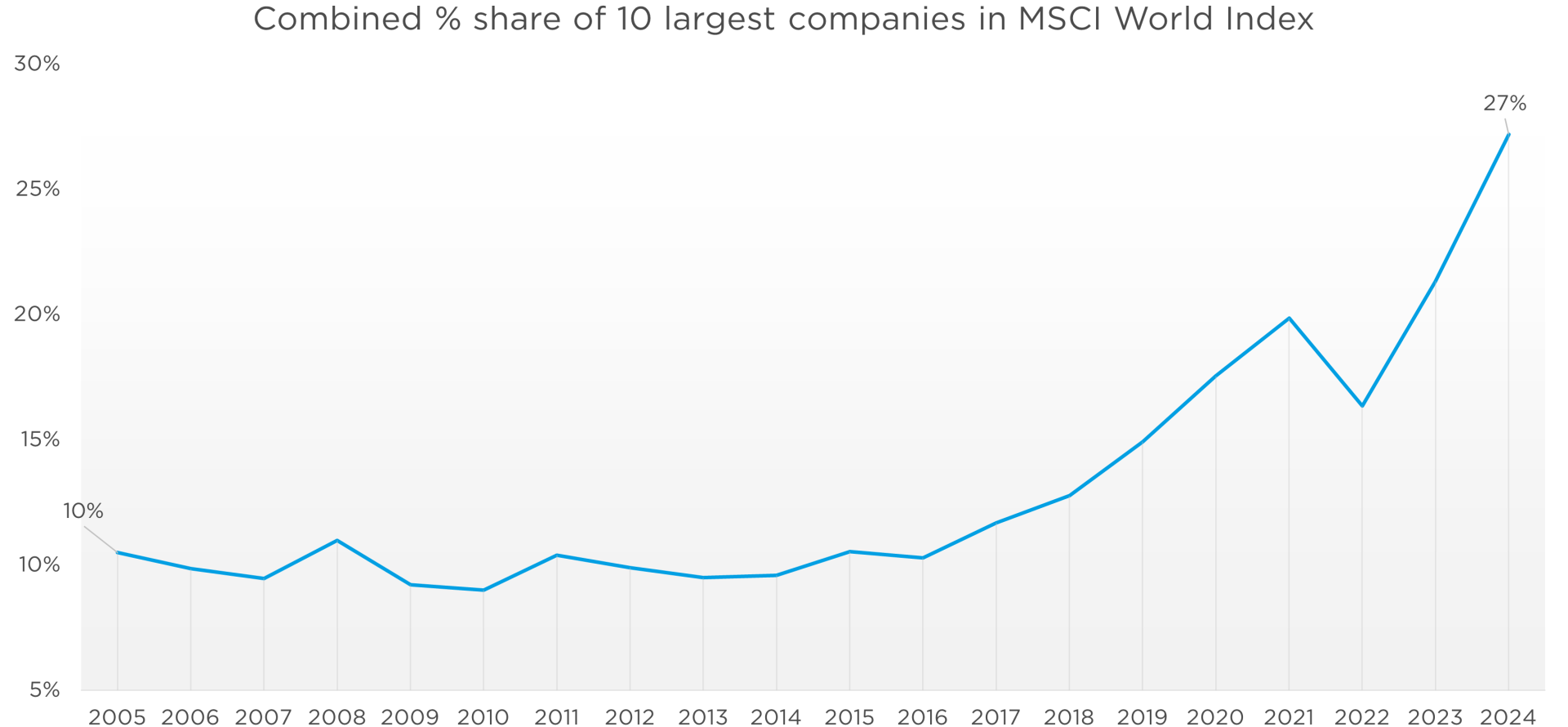

But these days, investors who track an index can find themselves with large positions in single stocks. The problem with concentrated positions in, e.g., NVIDIA, is that investors can see $600 billion of market value wiped out in a single day, as happened in January.

Figure 1: Concentration, not diversification

Source: CCLA, MSCI, monthly data 31 January 2005- 31 December 2024

Remember the 2000s, when Cisco was the world’s most valuable company, and its network technology ushered in ‘a new era of computing’? Networks remain a key technology today, but Cisco’s value is 57% lower than its peak value at the time. NVIDIA may be as revolutionary as Cisco was in the 2000s. But that doesn’t mean you need to hold as much of it as the index does.

Instead, there are diversified ways to capitalise on trends like AI (artificial intelligence). At CCLA, we don’t build portfolios based on an index. Instead, we believe that a company’s quality and persistent earnings growth drive its share price in the long run.

How to capture quality, at a reasonable price

So, how do we identify ‘quality’ shares? In information technology and AI, we look at four measures.

- Sector leadership. In many segments of IT, the market leader takes around 80% of that segment’s profits. The leading firm’s large customer base often translates into network effects and higher profitability than its competitors. That’s why we prefer, for example, chip manufacturer TSMC over GlobalFoundries, ecommerce firm Amazon over eBay, and, in IT consulting, Accenture over Capgemini.

- Superior revenue growth. We look at how a company can grow faster than its current market. For example: where a company offers cloud-based software, we analyse how much of its market is still ‘on-premise’, not in the cloud. In other situations, we identify companies that excel at creating new products, closely related to their existing ones, for their existing client base. That’s why we like, for example, business automation firm ServiceNow and design automation firm Synopsys.

- Financial performance. IT businesses benefit from economies of scale. So we look for improving margins and improving cash flow return on investment (‘CFROI’) over time. We like, for example, how cybersecurity provider Fortinet has expanded its margins over the years. Better margins have boosted the company’s earnings and its share price.

- Disciplined valuation. We avoid the speculative end of the market. Instead, we focus on companies with positive free cash flows that trade at reasonable valuations. Even if a company scores high marks on sector leadership, growth or ROI, we will not overpay for it. For that reason, we’re not invested in quality companies like Spotify, Cloudflare or cybersecurity firm CrowdStrike.

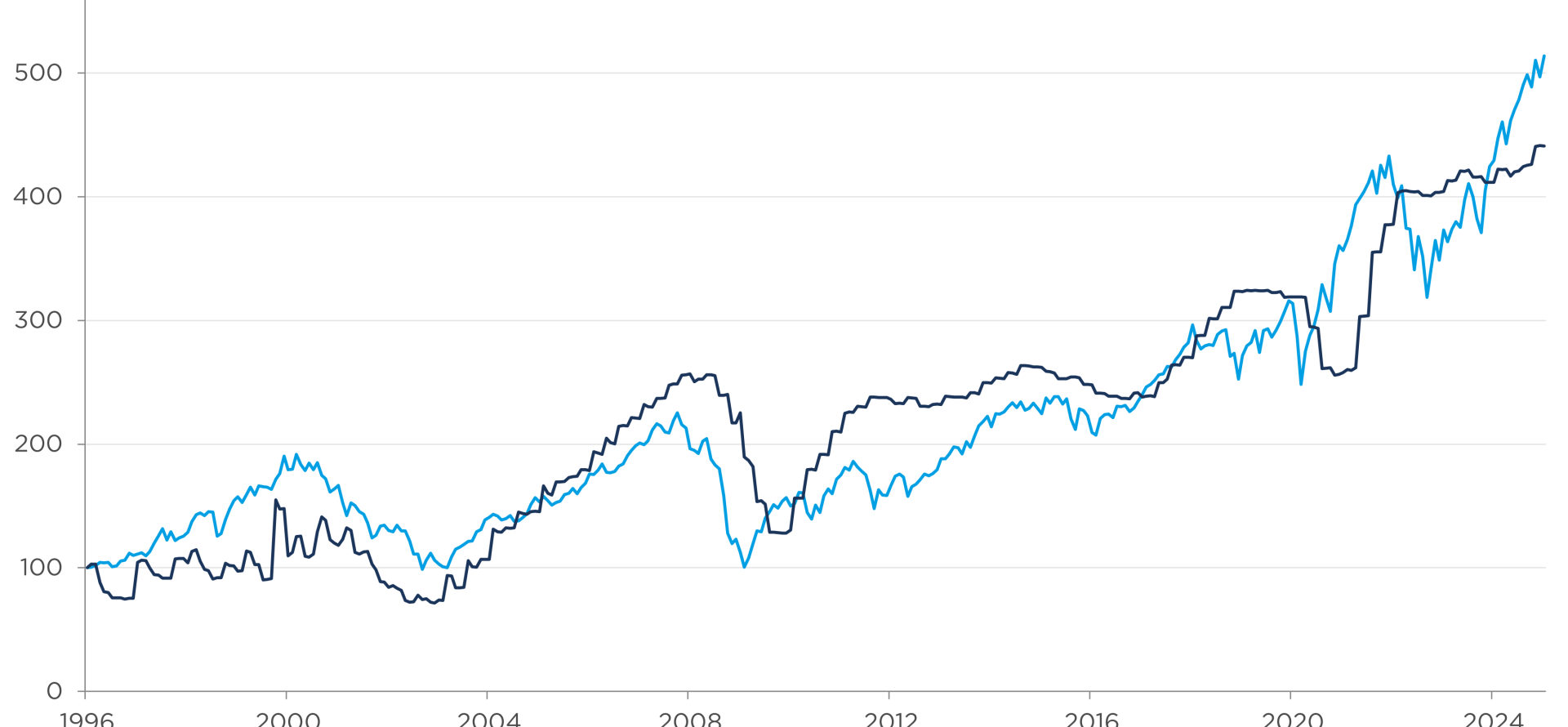

Finally, a company’s fundamentals, such as its earnings and ROI, are key to its share price. That’s not always true in the short run. But in the long run, companies with ‘quality’ fundamentals have a competitive advantage. They grow more quickly than their competitors and generate more cash.

Figure 2: Company fundamentals are key to share prices in the long run

Source: MSCI, CCLA, as of 31 January 2025. Note: We define ‘trailing EPS’ as earnings per share over the preceding 12 months. Both indices are rebased to the value of 100 as of 1 January 1996.

A broader universe than the index – tilted to quality, at a reasonable price

Because we’re interested in long-term performance, our portfolios don’t track the index. So what does the IT universe look like through our quality lens?

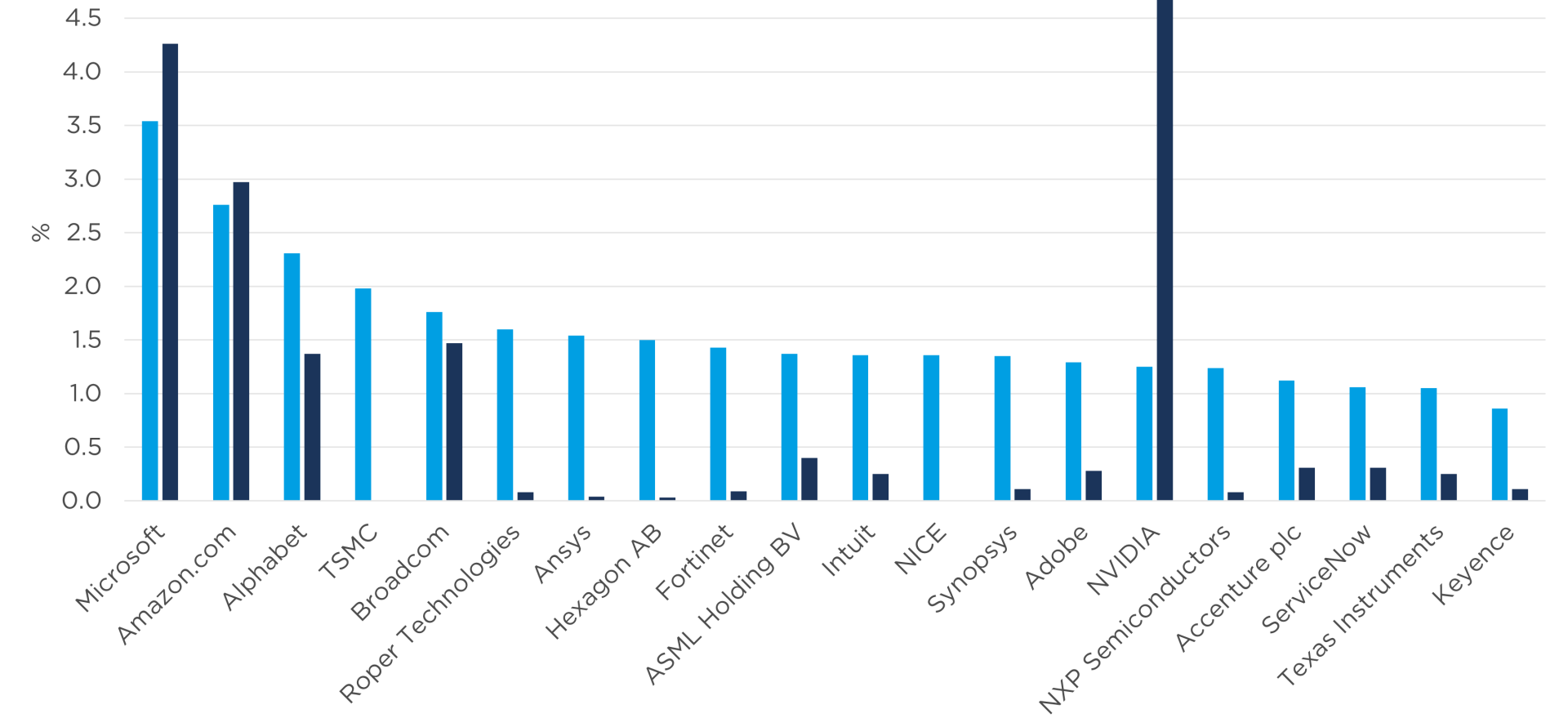

Figure 3: Quality, at a reasonable price

Source: CCLA Better World Global Equity Fund, MSCI, as of 31 December 2024. MSCI categorises Google parent Alphabet in its communications sector and retailer Amazon in its consumer discretionary sector.

Firstly, we remain enthusiastic about IT and AI! That’s why the companies in the figure above represent 32% of our Better World Global Equity Fund, versus 30% in the MSCI World Index. But despite our overweight, our portfolio is more diversified than the index. Our five largest holdings above account for 12% of the fund, versus 15% for the five largest IT positions in the index.

Secondly, our significant underweight in NVIDIA stands out. Instead, we hold a broader range of AI firms than the index. Our holdings include ASML, a near-monopoly in the semiconductor industry; Synopsys, the leader in electronic design automation (EDA); Broadcom, which helps Google, Meta and ByteDance develop proprietary chips; and TSMC, the world’s leading outsourced chip producer. In addition, we hold Microsoft, Amazon and Alphabet in part because they’re leaders in cloud computing and AI.

In summary: investing in quality at a reasonable price tilts our positions away from recent market favourites. Instead, we hold a wider range of segment leaders that generate significant cash, at reasonable valuations.

Capturing the AI trend, without the overhang

IT goes through innovation cycles, where winners first emerge in semiconductors, then in infrastructure and finally in software and services. For example: during the mobile phone revolution, chip producer Qualcomm was one of the earliest beneficiaries. Momentum then moved to phone manufacturers like Samsung and Apple. Finally, service providers like Google and Amazon became dominant.

We believe that AI is no different. Semiconductors are the foundation of the AI revolution, so NVIDIA dominates – for now. But we see the value of AI migrating to cloud infrastructure, such as Microsoft Azure and Amazon Web Services. From there, software and service providers like OpenAI or another new player may well take over.

Innovation naturally transitions from one part of the value chain to the next. For that reason, a large investment in a single share, as large as the current index weight in NVIDIA, has often been a bad idea.

Important information

This communication is issued for information purposes only. It does not constitute the provision of financial, investment or other professional advice. The opinions and analysis in this document represent CCLA’s house view and should not be relied on to form the basis of any investment decisions. Such opinions, expectations and/or projections may be subject to change at any time. CCLA undertakes no obligation to update or revise these. Actual results could differ materially from those anticipated. Any organisations, financial instrument or products described in this material are mentioned for reference purposes only which should not be considered a recommendation for their purchase or sale. Neither the Company nor the authors shall be liable to any person for any action taken on the basis of the information provided. CCLA strongly recommends you get independent professional advice before investing.

To ensure you understand whether a fund is suitable, please read the key investor information document and prospectus. The sustainability approach for each of our funds is outlined in its consumer-facing disclosure document. Past performance is not a reliable indicator of future results. The value of investments and the income derived from them may fall as well as rise. Investors may not get back the amount originally invested and may lose money.