3 April 2025

Tariffs are stagflationary. They lower growth and raise prices in the short term. Stagflation is bad for risk assets, especially equity and bonds – the 1970s attest to that.

We cut overall equity risk in mid-March

We cut the equity weight in our investment funds1 from 75% to 70% three weeks ago, specifically on our fears for a trade war. Instead, we reinvested 2 percentage points in the 2026 and 2027 maturities of index-linked gilts and kept 3 percentage points in cash. We did not increase duration risk in the funds by buying longer-dated bonds. With US inflation no longer decelerating, and with the inflationary impact of tariffs, we cannot see the Federal Reserve (Fed) make the cuts to the Fed funds rate that the market currently prices in.

We have also been re-cycling capital from the US into Europe

Over the last 12 months, our general trend has been to reduce exposure in the US and increase exposure in Europe. Our US equity weight has fallen from 70% to 62%, whilst exposure to Europe (including the UK) has risen from 26% to 36%. Within sectors that are likely to see some of the largest impacts, such as Consumer Discretionary, we have been tilting portfolios towards more defensive stocks. For example, we have sold Nike and added Compass Group.

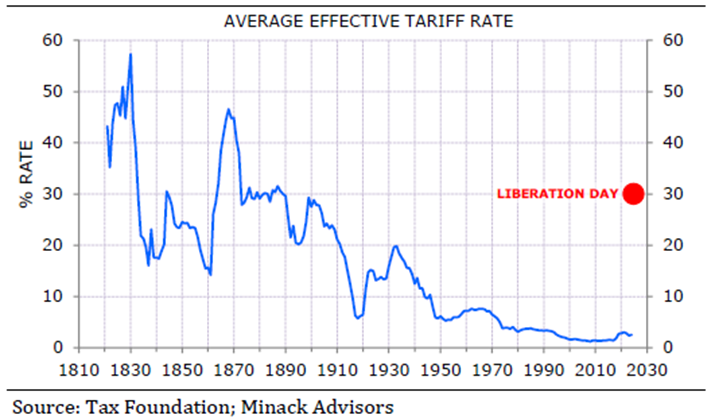

The tariff announcement

The incremental tariffs announced on 2 April were larger than the market had expected. The average US tariff rate was 3% before Trump’s election (according to Yale University2). It rose to 10% with the hikes to China, Mexico and Canada tariffs. And one early estimate after yesterday’s announcement has them now at 30%. This puts US tariffs at a 120-year high and compares with a 20% average tariff after the Smoot-Hawley Tariff Act of 1930. (Trump actually referred to this Act in his speech, saying that it had come too late to save the US economy from falling into depression. Many economists think of Smoot-Hawley as a contributory factor causing the depression.)

Market impact

Equity prices fell, as was to be expected. US Treasury prices rallied, which suggests the market is factoring in a higher chance of a recession and believes the Fed will cut interest rates. Four full 25 bps cuts are now priced into the forward curve, by April next year. The US dollar weakened. This is not what is supposed to happen, but it is what Donald Trump wants.

What next for our risk level?

The question is: should we do more to cut risk? We are mindful that equity bull markets normally run from recession to recession. So, unless this is indeed the start of a US recession, it is unlikely to be the peak of this equity market cycle. Our current view is that there is enough cushion in US growth to avoid a recession, so we are more likely to be adding risk back into the investment funds than cutting further. However, we will have to see what the international reaction is to this initial move. So far, that reaction seems restrained, with policymakers wanting to avoid an all-out trade war. If that view looks like changing, though, we will cut our equity weight further, to 65% and possible even as far as 60%. Instead, we would buy more index-linked bonds, possibly of longer duration (as the Fed would then cut interest rates).

What next for the equity book?

We are unlikely to make any large and immediate changes to our equity stock selection following Trump’s announcement this week.

The luxury goods industry is an obvious area where perceived impacts could be high. However, when we analyse the detail, the impact to a business such as luxury fashion house Hermès, which we hold in the investment funds, is manageable. Hermès’ gross margins are near 70% and its US sales account for 20% of revenue. We estimate that Trump’s tariff announcements would impact the company’s profits by just 2%, whilst a price increase of just 6% would be required to mitigate the impact – perfectly manageable for their clientele.

The CCLA investment funds also have high exposure, across sectors, to parts of the market where the direct impacts of tariffs are non-existent and where second-order impacts from potentially lower growth should be manageable. The financial industry is a good example. In this sector, our exposure is skewed towards exchanges, data & analytics businesses and insurance brokers that do not sell goods. Revenue visibility in these businesses is high, with multi-year contracts and a high proportion of recurring revenue. Our high software exposure in the information technology sector also has limited direct impacts from tariffs. Health care, too, should fare better, especially given that the industry has already been through its own idiosyncratic cycle.

Keeping our focus on quality

As we look forward into a world where uncertainty is high and tariffs loom over the global economy, it will be more important than ever to focus on high-quality businesses whose growth doesn’t solely rely on the economic cycle. High-quality businesses typically have higher margins, so higher costs because of tariffs will naturally have less of an impact on their profits. Similarly, quality businesses have pricing power and a greater ability to pass higher costs on to customers. Lastly, focussing on structural growth, rather than cyclical growth, should stand the investment funds in good stead if the economic situation deteriorates further.