27 August 2024

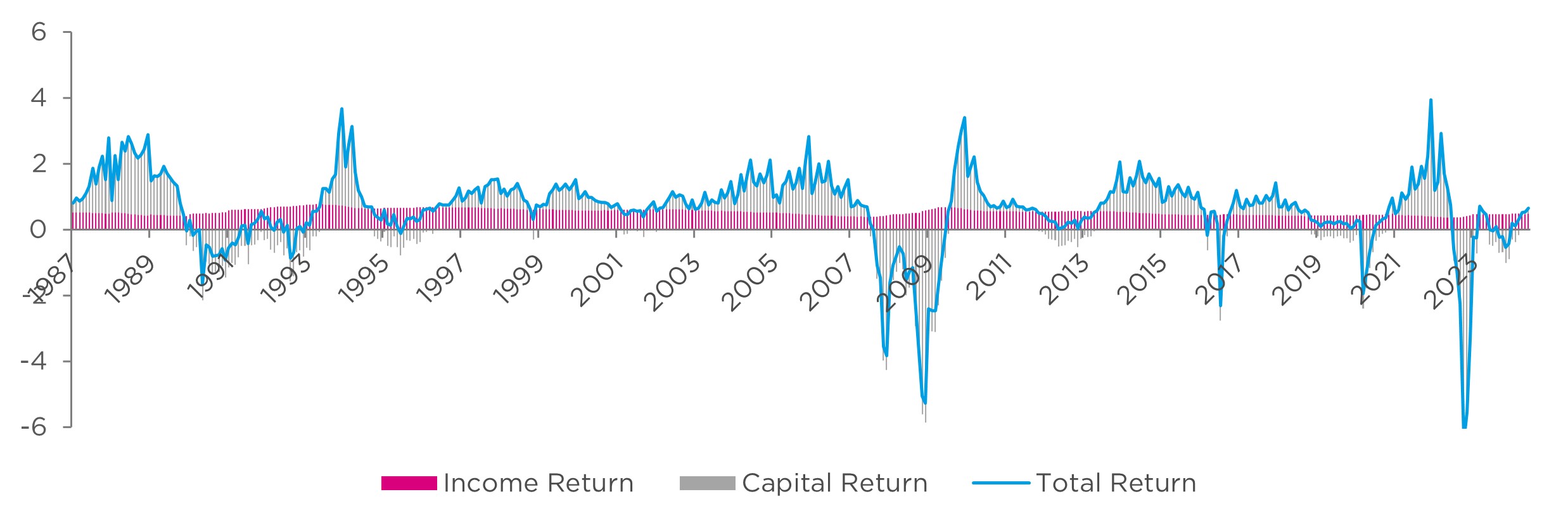

Capital return vs income return

UK commercial property is an asset class where long-term returns are dominated by the underlying income generation. Income (rent) from a property investment is generated from the tenant’s obligations specified in a lease, which are commercial contracts and usually long term, often spanning several years, providing a stable and predictable income stream for property owners.

The underlying relative stability of property income returns, compared with capital returns, is shown in Figure 1 for the MSCI UK Monthly Property Index. Since the inception of this index in 1987, commercial property has provided annualised returns of over 8%, of which rents contributed approximately 6.7% of the total return.

Figure 1: UK property investment returns since 1987

Source: MSCI UK Monthly Property Index, as at 30 June 2024. Past performance is not a reliable indicator of future returns.

Capital values at the low point?

Could commercial property net asset values be bottoming out now? Capital values are approximately 20% off all-time highs following the decline in the UK real estate market in 2022–23, driven by the rise in both long-term and short-term policy interest rates in 2022. The consensus is property yields are now at or close to the peak, with risks becoming more balanced and market expectations now turning to interest rate cuts rather than further rises. An inflection point in capital values could be at hand.

It is notable that investment market transaction volumes in UK real estate assets fell by 40% in 2023 compared to 2022 according to LSH1, as the market reacted to the higher interest rate environment and stressed sellers, in many cases, exited the market. Weak market conditions characterised by historically low transaction volumes became entrenched, but evidence is emerging of a slow recovery, particularly in the prime end of the market, whilst occupier market conditions and rental growth remains supportive, which is a sign of fundamental health and overall sentiment improving. However, for the time being, both buyers and sellers remain cautious.

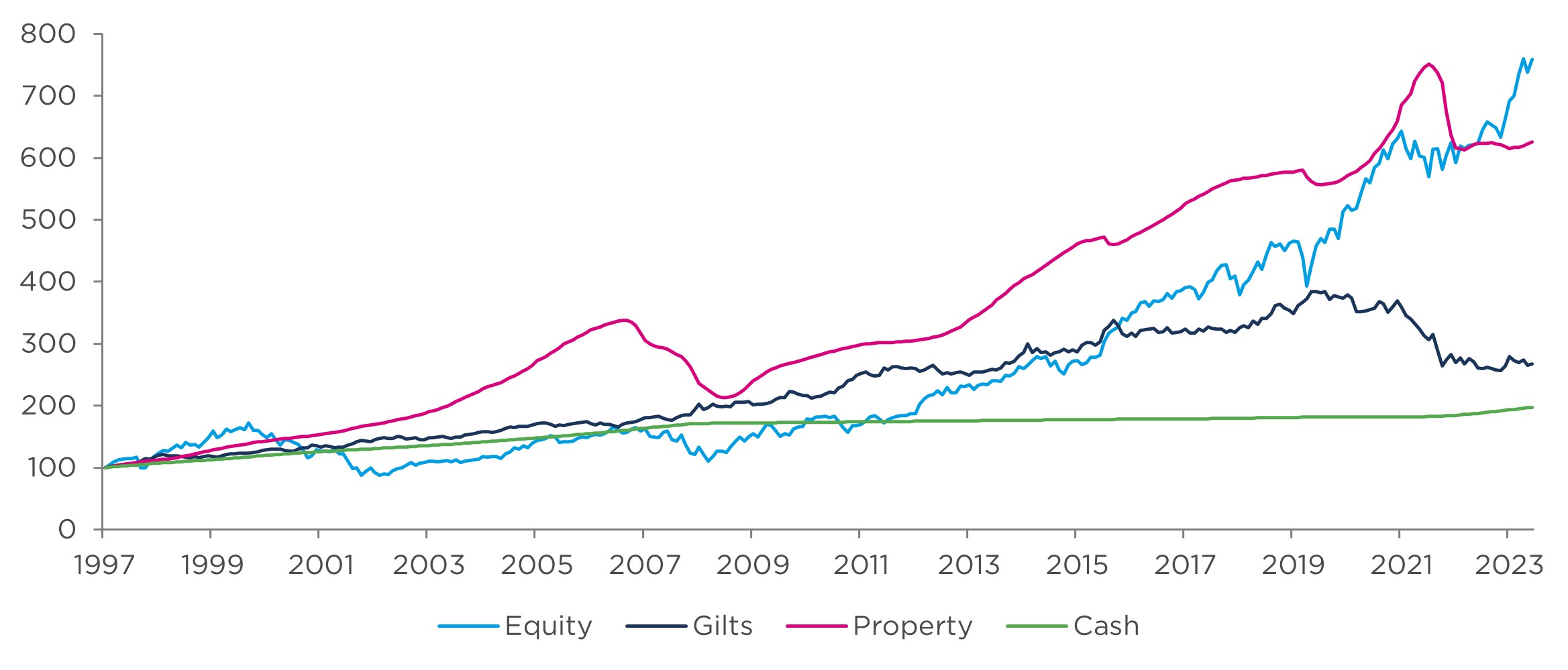

Figure 2 shows the total return of property against the major asset classes since 1997. Property has generated similar returns to global equity over the last 25 years, and considerably outperformed both gilts and cash. Property has also experienced much lower volatility of returns than global equity, at 10.1% versus 14.9% over this period.

Figure 2: Long-term total returns

Sources: 25 Years of Return, All Property Monthly TR Index (Property), Bloomberg for MSCI World GBP Index (Equity), iBoxx Sterling Gilts Index (Gilts) and UK Base Rate (Cash), as at May 2024. Past performance is not a reliable indicator of future returns.

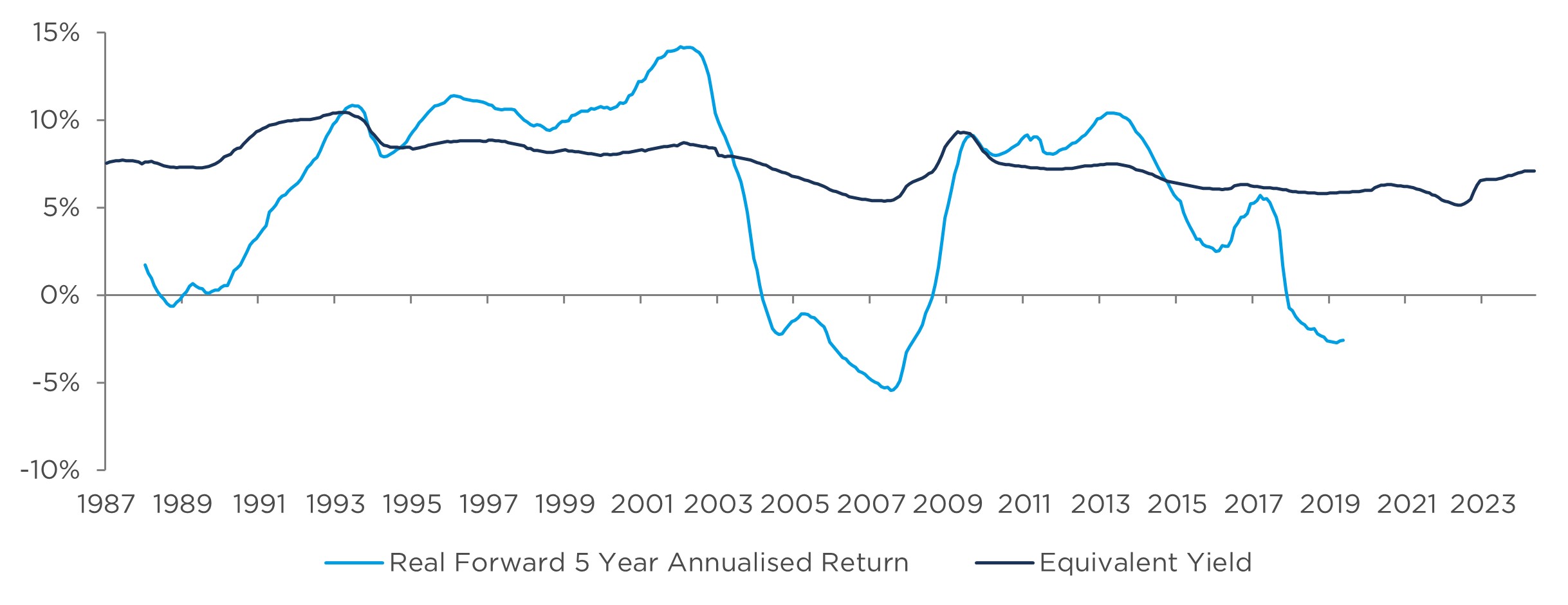

Forward returns

We use the property equivalent yield as the best single measure of the likely return to be derived from the property sector. The equivalent yield is a weighted average of the net initial yield and reversionary yield and represents the return a property is expected to produce assuming no growth but based upon the current income stream and the estimated rental value (ERV), and the timing of that income being received and secured. In other words, it captures the initial income yield and the likely changes in income levels over the lease term, triggered by lease events (i.e. lease expiry or rent review) which allows the income to reset to current market levels. Just as a government bond yield is a reasonably accurate predictor of future bond returns, the equivalent yield averages out around the realised forward property returns. Figure 3 shows this relationship – while there is more variability from year to year in the relationship, the average annual return of 8.1% nominal/5.7% real is close to the average equivalent yield of 7.5% over the same period.

Figure 3: MSCI UK Monthly Property Index Equivalent Yield vs rolling five-year annualised real total returns

Source: MSCI UK Monthly Property Index, as at 30 June 2024. Past performance is not a reliable indicator of future returns.

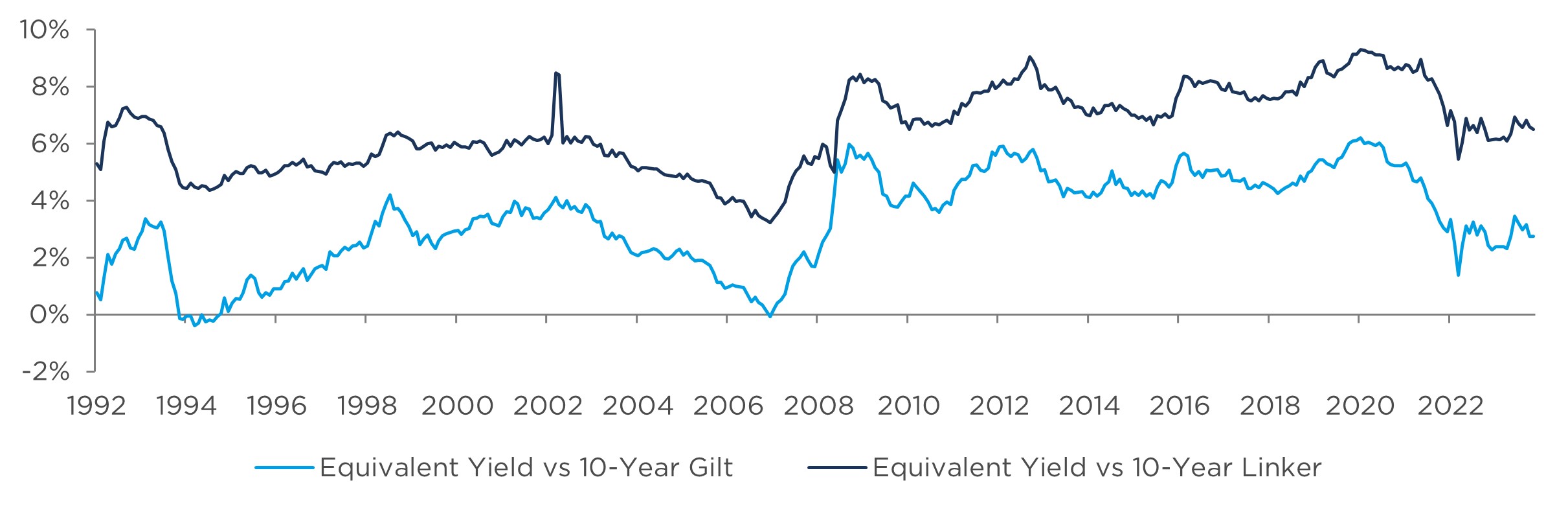

The property risk premium

We view the equivalent yield as a real yield measure, in the way that a conventional government bond yield is not. Government bond coupons are fixed, so have no protection from rising inflation, unlike linkers which clearly do have inflation protection, with both the principal and the coupon varying with inflation.

Therefore, it is appropriate to compare the equivalent yield with the real bond yield in order to assess relative value across the two asset classes over the longer term, even if the short-term relationship is not perfect and will reflect the timing of uneven rates of rental growth that will drive the equivalent yield relative to the initial yield. In Figure 4, the grey line is the spread between equivalent yield and the 10-year linker. What we see is that the spread is around 6% now, which is the high end of the 4–6% range that was in place before the Global Financial Crisis (GFC) of 2008–9, but at the lower end of the 6–8% range that was in place between the GFC and the pandemic of 2020, during which time zero interest rate policies (ZIRP) were in place at all the major G7 central banks. Which comparison is more relevant? We think the pre-GFC period is more relevant. Interest rates have normalised back to pre-GFC levels, or closer to pre-GFC levels, and we are of the view that we are not going back to ZIRP any time soon.

On this basis, we think a 600bps spread over real gilt yields offers an attractive risk premium.

Figure 4: MSCI UK All Property Index – equivalent yield spreads

Source: MSCI UK Monthly Property Fund Index as at June 2024. Past performance is not a reliable indicator of future returns.

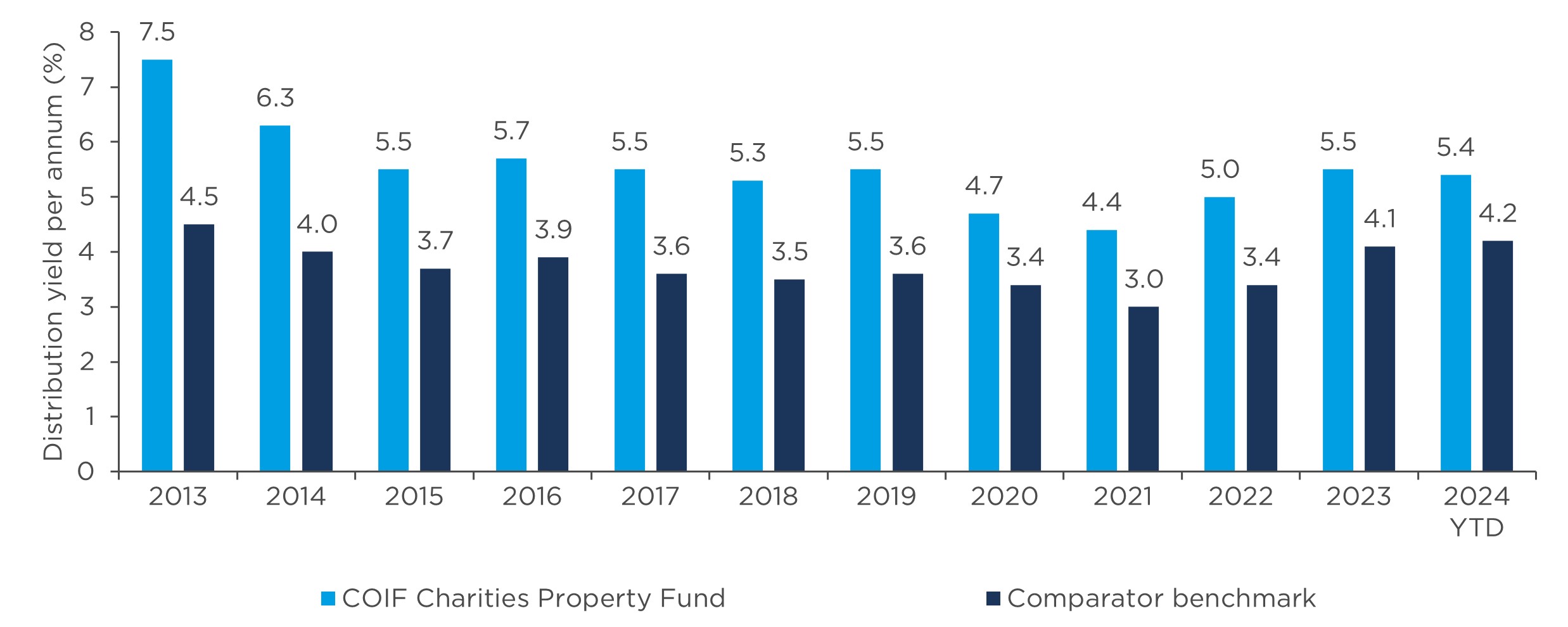

Figure 5 compares the distribution yield of the COIF Charities Property Fund to the MSCI UK Other Balanced Open-Ended Property Fund index, showing the historical yield pick-up available in the Fund versus the Benchmark. The current spread is narrower than it has been, but still a substantial 1.2% points.

Figure 5: Consistent, above average distribution yield

Source: CCLA and MSCI, as at 30 June 2024. Comparator benchmark: MSCI UK Other Balanced Property Fund Index. Past income yields are not a reliable indicator of future results.

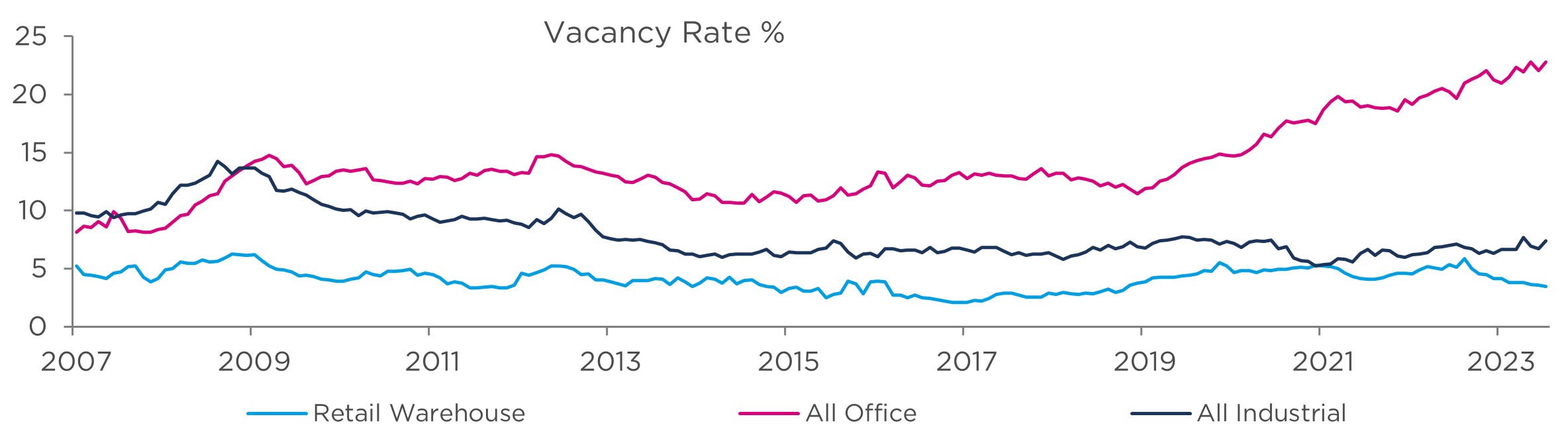

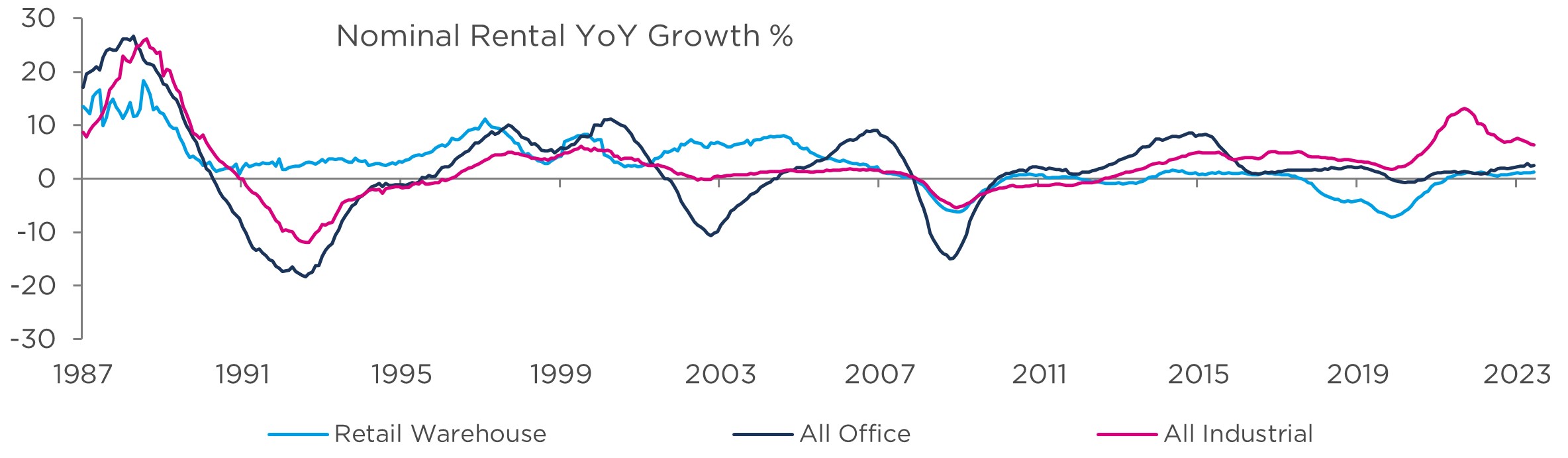

Vacancies and rents

We have seen a significant divergence in vacancy rates and nominal rental growth across different commercial property sectors. Figure 6 shows the current vacancy rates are relatively low and stable for both the retail warehouses and industrials sectors, with a steady rise in vacancy rates in office assets following the Covid-19 pandemic.

Looking at nominal rental growth, we are starting to see a convergence towards low single digit year-over-year growth across the retail warehouse, office, and industrials sector – enough to keep up with expected inflation, we would think.

Figure 6: Vacancy rates and nominal rental value YoY growth %

Source: Vacancy Rate and Nominal Rental Value charts: MSCI UK Monthly Property Index as at June 2024.

Risk factors – illiquidity and forced redemption

In our view over the last six months there has been a shift in the market mindset, from predominantly capital value risk to illiquidity risk. In 2022-3, capital values were perceived to be at risk of further decline given inflation and interest rate risk remained high. Today there is less concern about interest rates, inflation and therefore capital values, and more focus on the role less liquid assets such as property play in a portfolio. Many property funds have lengthened their redemption notice periods, and some have even gone as far as to gate existing investors to prevent redemptions.

CCLA extended the redemption notice period for our three property funds from 90 days to six months in October 2022, with the aim of providing a sufficient period to sell assets at market value, rather than at a discount, as forced sales would be to the detriment of all investors. We continue to evaluate market liquidity and will revise the redemption period when the market allows. Asset disposals have focused on those assets which we believe have become less attractive and less well placed to support the Funds’ income and capital growth over the long term.

Conclusion – asset class at the trough, investor sentiment to follow

Where we are today is a market where property fund NAVs have largely stopped falling, where the next moves in interest rates are expected to be down rather than up, where transaction volumes are normalising and fears about fund liquidity are also slowly receding. Starting equivalent yields for the UK commercial property sector point to decent forward real total returns to the sector, based on an attractive initial yield relative to historical levels. Our guess is that the asset class is at or very close to its trough and that investor sentiment will follow, with a lag.

1 Source: Lambert Smith Hampton, April 2024.

Important information

This document is produced for professional investors and is also available on request.

This document is not intended for general retail public distribution and must NOT be distributed to other persons without CCLA’s permission.

This document is issued for information purposes only. It does not constitute the provision of financial, investment or other professional advice and does not constitute an offer or invitation to make an investment in any financial instrument or in any CCLA product.

The market review and analysis contained in this document represent CCLA’s house view and should not be relied upon to form the basis of any investment decisions.

Any forward-looking statements are based upon CCLA’s current opinions, expectations and projections. Such opinions, expectations or projections may be subject to change at any time. CCLA undertakes no obligation to update or revise these. Actual results could differ materially from those anticipated.

Past performance is not a reliable indicator of future results. The value of investments and the income derived from them may fall as well as rise. Investors may not get back the amount originally invested and may lose money.

CCLA Investment Management Limited (registered in England and Wales, number 2183088), whose registered address is: One Angel Lane, London, EC4R 3AB, is authorised and regulated by the Financial Conduct Authority.