30 August 2023

Now that the Bank of England has woken from its slumber and raised interest rates (14 times and counting) it’s worth asking the question ‘what’s a fair interest rate?’

There are lots of ways of thinking about this, but perhaps the most obvious is, how much interest would you expect to receive on cash deposited at your bank? According to the Bank of England the rate received on ISA deposits is currently a measly 2.5%. That’s measly because the Bank’s policy interest rate is 5.25%, and a five-year fixed (95% LTV) mortgage will cost you 6.29%. Someone is making a lot of money from these spreads, and it’s clearly not the consumer. (Psst - it’s the banks). But there’s clearly a difference between what you would expect to receive and what you do receive, so this doesn’t get us any nearer to understanding what a fair interest rate is.

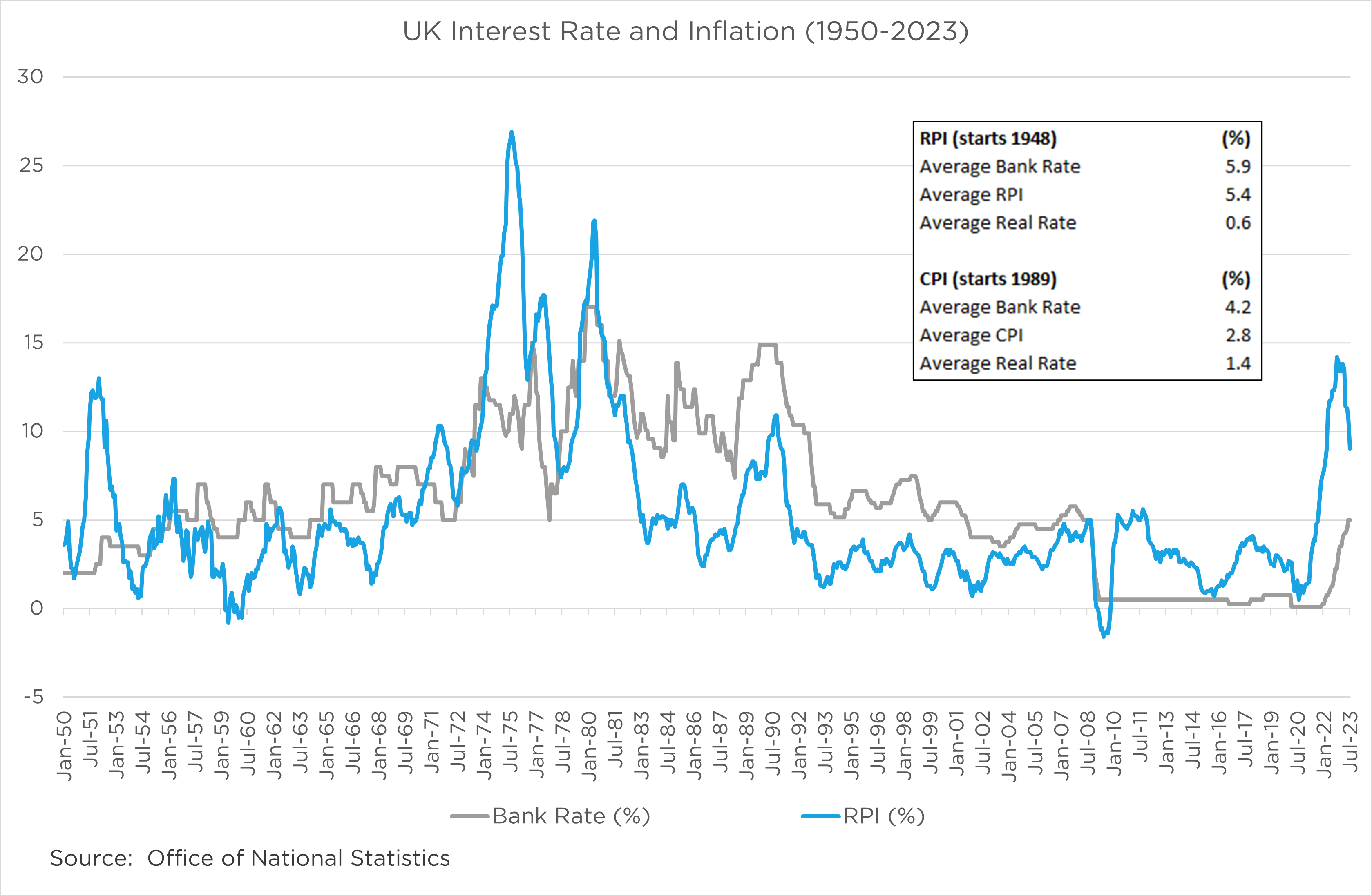

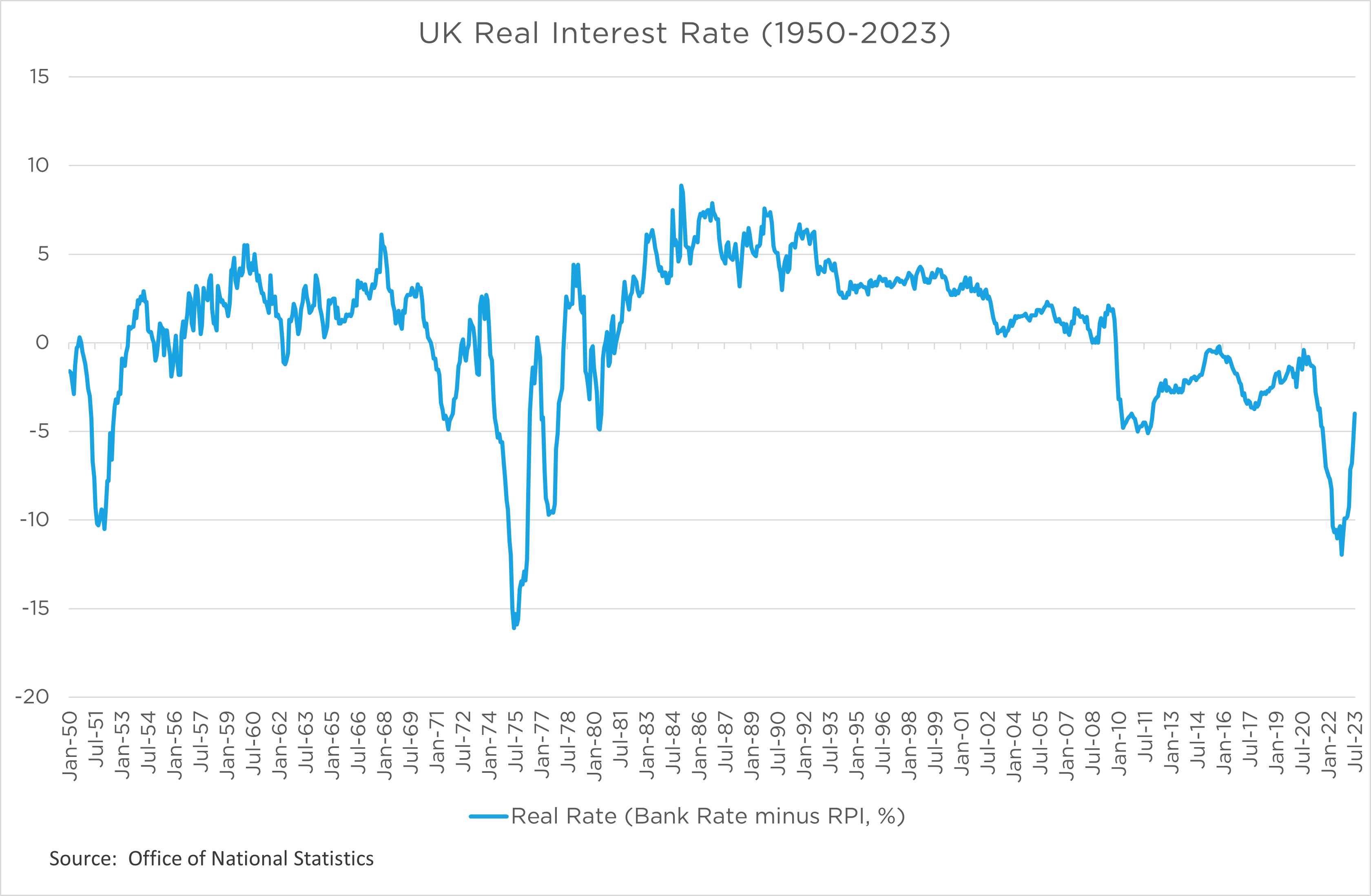

Another way of thinking about it is to look at history. The chart below left shows Bank rate and inflation back to 1948, and below right we show one minus the other, aka the real interest rate. What stands out is that real interest rates have fluctuated wildly. There have been long periods (decades) when real interest rates were 0 to 5% interspersed with long periods (again, decades) when they were 0 to -10%. We do observe that the long run average real interest rate has been 0.6% (since 1948) but more recently has been higher at 1.4%. However, the volatile history makes it impossible to draw firm conclusions.

How would an economist answer the question? Well most likely they would think about the natural rate of interest, which rejoices in the jargon name ‘r-star’ (or r*). The natural rate is the rate which equilibrates between savings and investment. So it’s the level that sees full employment and stable inflation. And it’s usually calculated taking into account the trend real growth rate of the economy and adjusting for savings and investment propensities. As it’s a real term, one then adds trend inflation to get to an equilibrium nominal interest rate.

When we plug our assumptions into this framework today, we get something like this. Trend real growth rate: 1.5%. Long-term inflation expectation: 2.5%. Finally, since we think savings propensity will fall as the population ages and demand for investment will rise as infrastructure is refreshed in the energy transition, this should put upward pressure on real interest rates, so we add another 0.5% to account for that. Adding these up we get a real interest rate of 2.0% and a nominal interest rate of 4.5%.

So there’s our answer: 4.5% is a fair UK interest rate.

If this guesstimate is even close to correct, we can go a step further and make a statement about how loose or tight monetary policy is. The Bank Rate is 5.25%, so it’s 0.75% above our guess of the neutral rate. We can say that policy is a little tight, as well it might be with CPI inflation still 7% (albeit falling fast). Market expectations for Bank rate to go over 6% early next year would entail what we would call tight policy. Again that may not be wrong given still high inflation and full employment. But the market expectation that the policy rate will still be over 4.5% (i.e. what we would call tight) in three years’ time? Now that really does feel wrong, and it’s why we have been slowly buying gilts.

Please refer to the glossary on our website for explanations of terms used in this article.

This document is issued for information purposes only. It does not constitute the provision of financial, investment or other professional advice and does not constitute an offer or invitation to make an investment in any financial instrument or in any CCLA product.

The market review and analysis contained in this document represent CCLA’s house view and should not be relied upon to form the basis of any investment decisions.

Any forward-looking statements are based upon CCLA’s current opinions, expectations and projections. Such opinions, expectations or projections may be subject to change at any time. CCLA undertakes no obligation to update or revise these. Actual results could differ materially from those anticipated.

Past performance is not a reliable indicator of future results. The value of investments and the income derived from them may fall as well as rise. Investors may not get back the amount originally invested and may lose money.

CCLA Investment Management Limited (registered in England and Wales, number 2183088), registered address: One Angel Lane, London, EC4R 3AB, is authorised and regulated by the Financial Conduct Authority.