20 August 2020

CCLA’s response to the Charity Commission’s consultation

In March 2019, a group of charities wrote to the Charity Commission seeking ‘urgent clarification’ on the extent to which their investments should align with their charitable objectives.

There is currently no regulation to say that charities should have a responsible investment policy; and there is a widely held view that the law needs to be updated. Current Charity Commission CC14 guidance is based on the Bishop of Oxford case in 1992. Richard Harries, the bishop, challenged the Church Commissioners over their investment policy. The conclusion: ‘Most charities need money; and the more of it there is available the more trustees can seek to accomplish.’

Therefore, the purposes of the charity are usually best served by seeking a maximum return. This is the basis of the current guidance. Under CC14, trustees can decide to invest ethically, as long as one of the following reasons applies:

- A particular investment conflicts with the aims of the charity.

- The charity might lose supporters or beneficiaries if it does not invest ethically.

- There is no significant financial detriment.

The guidance is negative, vague and far from reassuring:

‘Trustees must ensure that any decision that they take about adopting an ethical investment approach can be justified within the criteria above. They must be clear about the reasons why certain companies or sectors are excluded or included. Trustees should also evaluate the effect of any proposed policy on potential investment returns and balance any

risk of lower returns against the risk of alienating support or damage to reputation. This cannot be an exact calculation but trustees will have to assess the risk to their charity.’

There are no examples of how, for instance, non-environmental charities can consider climate change in their investment policy. Although superficially unrelated, they are in fact intrinsically intertwined. Perceptions have changed.

In summary, our stance can be seen as a progressive reading of the current guidance:

- We believe it is no longer possible (or desirable) for charities to separate financial returns from their mission.

- Investment markets, and the returns that they can deliver, are only as healthy as the people, communities and environment that supports them. How we respond to these issues will dictate how economies – and portfolios – perform.

- Charities should have an obligation to incorporate environmental, social and governance (ESG) criteria into investment decision making and take steps to align financial assets with values and mission.

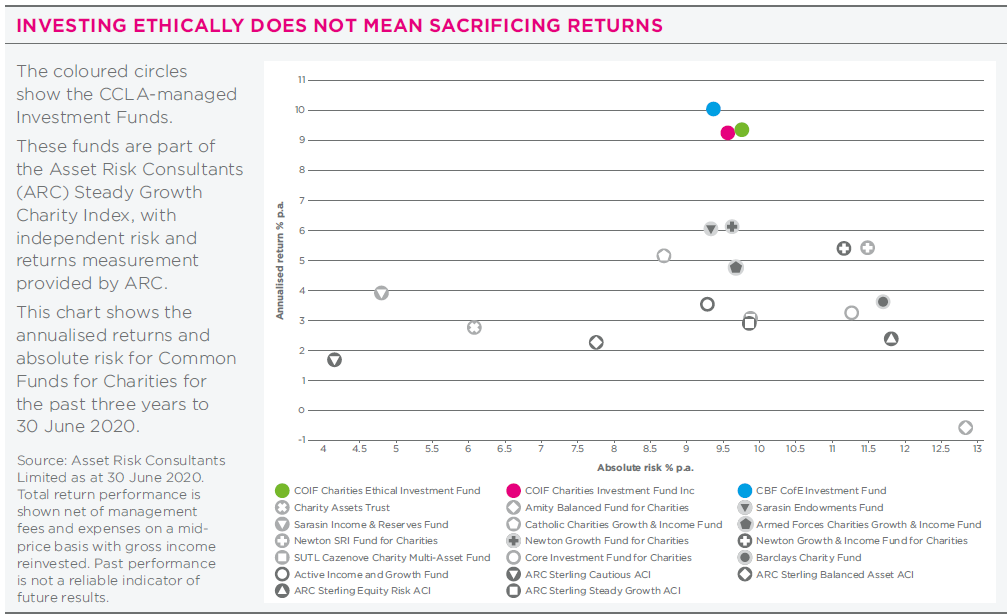

In practice, a simple performance comparison between CCLA’s two flagship multi-asset funds (the COIF Charities Investment Fund and the COIF Charities Ethical Investment Fund) should allay any fears that an increased emphasis on responsible investing will reduce returns. The broad ethical exclusionary policy applied to the Ethical Investment Fund has had no material impact on performance (see chart). In addition, we have large-scale engagement programmes in place to tackle some of the most pressing environmental and social problems that we face today. The debate continues. Some say that the Charity Commission should compel charities to invest sustainably. Others fear reputational risk and litigation that may come with a specific ruling. Once the Commission releases the new guidance, we will publish a comprehensive guide to responsible investing.

Investments and investment markets provide much needed funding for the charitable sector. At CCLA we manage approximately £10bn on behalf of over 35,000 not for profit organisations. The income delivered by these investments alone contributes approximately £217m to charities every year; this supports a substantial amount of good work.

Furthermore, over the past decade, charities and foundations have been at the forefront of exploring the different ways that investments can be used to deliver change. From Shareholder Activism to Programme Related or Mixed Motive investment we have seen countless examples of how social and environmental aims can be delivered through the creative use of financial resources. However, irrespective of how charities choose to invest their money, we agree that it is no longer possible, or desirable, for charities to separate the pursuit of investment returns from that of their mission. Instead, it is increasingly clear that investment markets, and the returns delivered by the businesses listed upon them, can only be as healthy as the communities and the environment that supports them. From climate change to the recovery from the COVID-19 public health crisis that has gripped the world as we write this submission, over the coming years and decades we face unprecedented social and environmental challenges. How we respond to these issues will dictate how global economies, and the investment portfolios that fund charitable activity, perform for years to come.

For this reason, we believe that as investors with unrivalled experience of delivering positive change charities have both a financial and missional obligation to incorporate environmental, social and governance (ESG) issues into investment decision making and to take steps to align their financial assets with their values and mission. To unleash the full transformative and creative power of the sector in this way, we believe that charity trustees will need a permissive regulatory framework that allows a variety of different approaches to investment. Therefore, we believe that trustees should face only two obligations when it comes to managing their charities’ financial assets:

- Trustees should have a duty to use their financial resources in a way that they believe will best help the charity achieve its purposes.

- They should report annually on how they have discharged this duty.

This would allow charities to use their assets, and reflect their charitable mission, in a wide variety of ways. This includes the prevalent ‘Invest and Fund’ model that permits charities to maximise their investment returns within an appropriate risk budget, to provide funding for their charitable operations.

As we expect ‘Invest and Fund’ will remain the predominant method adopted by trustees we believe that it would be beneficial for the Charity Commission to update their guidance to charities who use this approach. Specifically, we would encourage the Commission to:

a.

Clearly state that investment managers who act on behalf of charities must:

- Integrate ESG factors into their investment analysis and decisionmaking processes, in a way that is consistent with the charity’s real investment time horizon

- Encourage high standards of ESG performance in the companies that they invest in through voting and engagement

- Report on how they have implemented these commitments. As this relates to maximising investment performance, rather than aligning investments with the charity’s values, such a position would be in line with emerging best practice as adopted by other sectors (such as the Pensions Regulator), the findings of the UN Environment Programme Finance Initiative and Principles for Responsible Investment supported Fiduciary Duty in the 21st Century Project, and several leading charitable investors.

b.

Clarify that trustees of charities that have adopted the ‘Invest and Fund’ model have the ability to avoid investing in companies and sectors that they believe are detrimental to their charities’ purpose. This is in line with the 2015 Opinion produced by Christopher McCall QC.

c.

Encourage charities that use ‘Invest and Fund’ to take other steps to align their portfolio with their mission. As per the current CC14 guidance this can include instructing their investment manager to conduct shareholder activism, on issues that matter to the charity, with companies in their portfolio. Whilst a progressive reading of the existing CC14 guidance provides the ability for charities to invest in this manner, we believe that trustees would benefit from revised guidance providing them with the reassurance that they can be creative in how they use their resources to achieve their purpose.