At CCLA, we believe investors have a responsibility to drive positive change.

We believe that this is best achieved by pushing companies to do more to address the major challenges facing us today. From climate-change, nutrition and human rights to biodiversity, investors can make their voice heard and can make change happen.

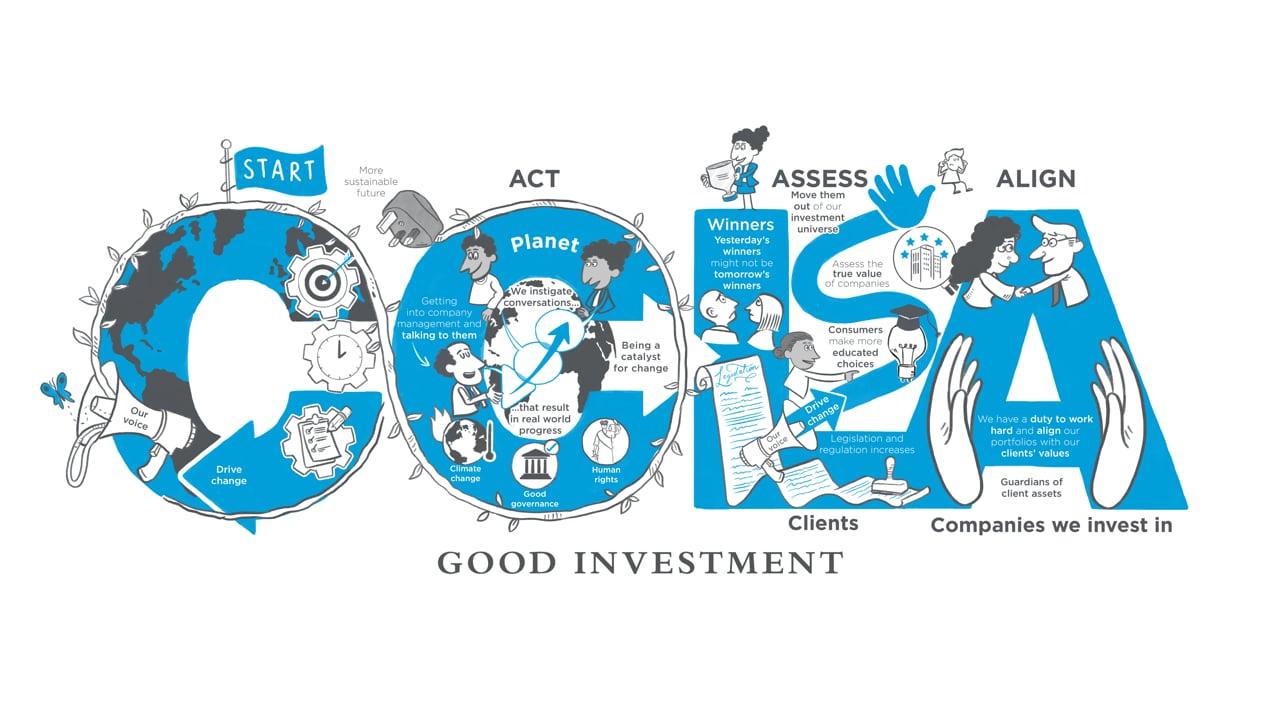

Good Investment

Our philosophy is Good Investment. So, what is Good Investment?

We aim to manage our clients’ investments in a way that aligns with their values and, for our not-for profit clients, furthers their mission. To do this we consider environmental, social and governance (ESG) factors in our listed equity investment process and go beyond the boundaries of traditional investor engagement to drive change.

This is summarised in our three guiding principles:

Act

We act as an agent for ‘change’ because investment markets can only ever be as healthy as the environment and communities that support them.

Assess

We assess ESG standards because we believe that a combination of legislation, regulation and changing societal preferences can impact negatively on the most unsustainable business models.

Align

We invest in a way that we believe is aligned with our clients, as we are the guardians, not the owners, of the assets we manage.

Better World stewardship report

Read how we are driving real-world change through active ownership and by engaging with companies on key issues facing society.

How responsible investment affects stock selection

We integrate ESG factors into our listed equity investment process with the aim of better understanding financial risks that the lens of conventional financial analysis may miss. Businesses involved in the most unsustainable activities are likely, over time, to be negatively impacted.

Before making an investment, we look at companies’ corporate governance, how they approach their most financially material sustainability risks, and whether they have been involved in any related controversies.

Once an investment has been made, we routinely monitor companies’ ESG characteristics to ensure that standards do not slip.

Industry recognition

What are the Sustainability Disclosure Requirements (SDRs)?

New ways of investing have given rise to a new vocabulary. One that includes terms like ESG (environmental, social and governance), impact investing, ethical investing, net zero, and sustainability.

To prevent confusion about these terms and mis-selling, the Financial Conduct Authority (FCA) has introduced Sustainability Disclosure Requirements (SDRs).

The key parts of the SDRs are:

1. An anti-greenwashing rule

Investment firms must be clear, fair and not misleading when they claim sustainability. Those claims must be consistent with the sustainability characteristics of the investment product they offer.

2. Investment labels

There are four investment labels that investment firms can attach to investment products; these are:

For funds that invest 70% or more of their assets in holdings that have the potential to improve environmental and/or social sustainability over time. E.g. companies that have committed to improving their business practices in relation to human rights.

For funds that invest 70% or more of their assets in holdings that aim to achieve pre-defined positive, measurable environmental or social impact. E.g. renewable power generation.

For funds that invest 70% or more of their assets in holdings that are environmentally and/or socially sustainable. E.g. sustainably managed forestry assets.

For funds that invest in accordance with two or more of the objectives above.

Providers must determine the sustainability objective of each labelled product, with robust, evidence-based standards that are an absolute measure of environmental and/or social sustainability.

3. Naming

The SDRs only allow funds to use the term ‘sustainable’ in their names if they have an investment label. Only funds with the ‘sustainability impact’ label can mention ‘impact’ in their names.

Funds without a label, however, can still use terms such as ‘green’, ‘socially responsible’, ‘carbon neutral’ etc. in their name, if at least 70% of their holdings align with those descriptions.

4. Marketing

Firms can only use sustainability-related terms in their marketing where this is consistent with the sustainability approach of the product.

Funds that use sustainability-related terms in their marketing but don’t use a sustainable investment label must state this. They must also state why they don’t use a label.

5. Sustainability reporting

Firms that use a label or sustainability-related terms without a label must produce a fund-level and firm-level report at least once a year .

CCLA will publish its first fund-level report by 2 December 2025 and its first firm-level report by 2 December 2026.

At CCLA, we believe we have a duty to help address systemic risks that threaten communities, the environment and investment markets themselves. For that reason, we welcome the SDRs and have taken action to implement them across all our funds.